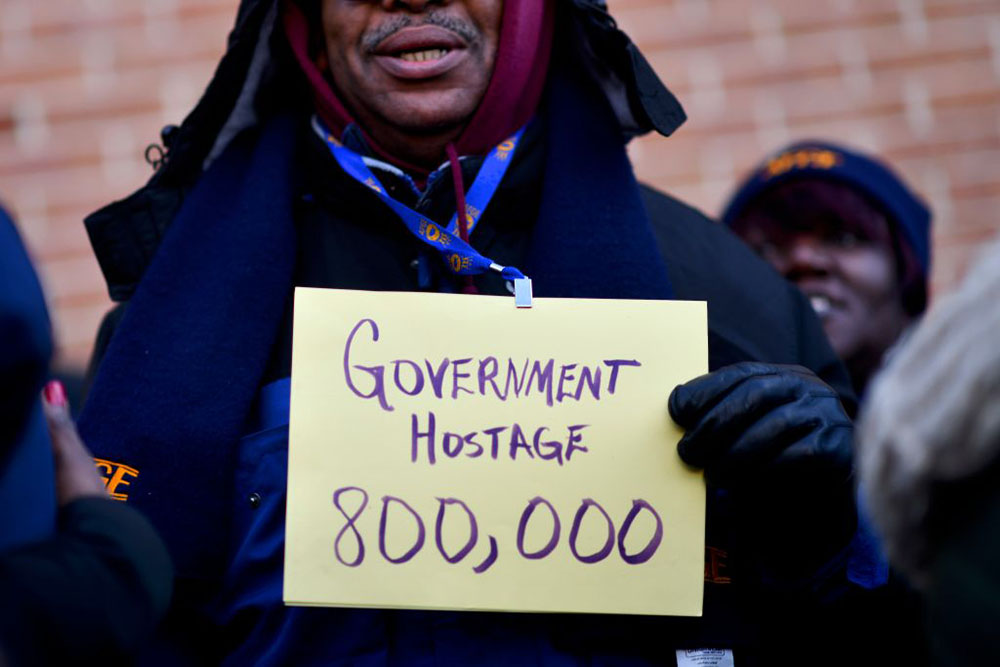

The federal government has reopened after the longest shutdown in history, which caused federal workers to miss two paychecks and cost the economy $11 billion dollars — $3 billion of which will never be recouped. The scariest part, though, might be that this horror show is starting to seem normal.

This is the third time the government has shut down in the last year and — unless President Donald Trump drops his demand for a border wall — everything from the national parks to the National Science Foundation could be closing up shop again on Feb. 16.

In the face of all that, America’s federal workers are thinking twice about their careers — and that’s bad for workers and the country.

Historically, the federal government (and public service writ large) has been a pretty good place to work. Not only does it allow people to serve their country (which many are keen on), it is the kind of quality job that all people should have. There is stability. There are retirement benefits. There is health care. There is paid leave. There is pay transparency. There is a union.

Get Talk Poverty In Your Inbox

Due in large part to the fact that the federal government has offered stable opportunities for advancement and a secure job with a steady paycheck, the federal workforce has disproportionately attracted people of color and people with disabilities. The latest data show that people of color are overrepresented in the federal government: More than 18 percent of workers in the federal government are black (compared to about 11 percent of the overall labor force) and Native Americans are more than one-and-a-half times as likely to work for the federal government than be in the overall labor force. Fourteen percent of full-time federal workers are people with disabilities, compared to 3.8 percent in the overall labor force. Veterans, who comprise nearly a third of the federal government, are also disproportionately represented.

But while federal jobs tick many of the job-quality boxes, satisfaction has been declining. The latest data reveal that morale at the Departments of Education and Health and Human Services fell by more than 10 percentage points between 2017 and 2018, and morale at the Consumer Financial Protection Bureau dropped by an astounding 25 percentage points.

One can only imagine what basement these numbers would be in if the survey happened this week.

This decline is likely due in no small part to the fact that attacks on federal workers have been mounting in recent years. Their work has been condescendingly dismissed by Trump, and National Economic Council Director Larry Kudlow referred to their unpaid efforts during the shutdown as “volunteering.” They have been asked to work with fewer staff due to hiring freezes and for diminishing wages due to Republican-pushed pay freezes.

Public sector unions have come under attack, both by Trump and the Supreme Court. And now workers have literally been forced to make do without pay, while many have still been having to show up and clock in. More and more work is being shifted to contractors who have fewer protections and who will likely not even be paid for the time they could not work during the shutdown. (Contractor satisfaction, which is likely even lower, deserves a whole article unto itself.)

Is it any wonder there have been reports of federal workers departing government service?

This could spell trouble, not just for the workers themselves who deserve far more than to be pawns in Trump’s racist game of chicken with the economy, but for our country in general. Reduced employee morale can lead to lower productivity — not a good thing when you’re trying to run a business, much less a country. We’ve also seen what it looks like when we don’t sufficiently invest in public services: lines get longer, corporations get away with defrauding the American people, and people die waiting for the services and benefits they need.

And if Trump’s divisiveness leads to less diversity within the workforce, the evidence indicates that could be bad for the public, too, because it matters who our public servants are. Research finds that having a diverse public labor force is important for the consideration of the interests of people of color in a range of circumstances. For example, having more black and Latino bureaucrats is related to having more Latinos and blacks judged eligible for rural housing loans. Having a larger share of black federal workers in the Equal Employment Opportunity Commission is positively related to the number of discrimination claims filed by black workers.

There are high costs to everyone when we treat federal workers like disposable widgets — and in the wake of the shutdown we may find out exactly how high they are.